2.22 Housing

Housing is a basic need. A well-functioning housing market, with a supply of accommodation to suit households at different stages of the lifecourse, underpins a successful economy. Housing together with essential public and social infrastructures (access transport, water and waste treatment capacity, schools, recreation) and services are essential for building sustainable communities.

Current difficulties in the housing market in Ireland are well-documented. There is limited supply in the housing stock across all tenure types (private ownership, private rental, social and affordable housing) and strong demand for housing. This situation is resulting in increased prices in house purchase and rents. These difficulties are present in the local housing market in Limerick.

House purchase and rental costs Limerick

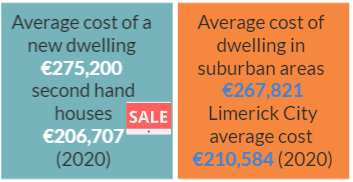

Based on analysis of house purchases in Limerick over the period 2008-2020, the average cost of a new dwelling in Limerick was €275,200 and €206,707 for second hand houses. Prices mainly increased from 2012 onwards with prices increases accelerating from 2018. Average price varies by location. They are highest in the Metropolitan Area, followed by Adare Rathkeale, Cappamore-Kilmallock and Newcastle West. Within the Metropolitan Area, prices are higher on average in the suburban areas -€267,821 on average in 2020 compared with €210,584 on average in the former Limerick City Council area).[1]

Since 2020, house prices have continued to increase nationally, and in the Mid-West and Limerick housing market. Between February 2021 and February 2022, national house prices increased by 15.3% and by 14.8% for the Mid-West.[2] In February 2022, average house prices for Limerick City were €222,000 and €231,000 for the former Limerick County. It is expected that the same sub-area differentials apply (Metropolitan Area versus rural Municipal Districts, city versus suburbs) as outli ned above.

ned above.

Average rental prices have also increased significantly but again show substantial variations across the territory. Areas within and with closer proximity to the city have higher rental costs. For instance, the average monthly rent (all property types) for Limerick City and County in 2020 was €892. For rentals within Limerick Metropolitan area, it was €1,026. Monthly rents were lower on average in Newcastle West MD at €616, €713 in Cappamore-Kilmallock and Adare-Rathkeale (€919). More recent data indicate that between Q4 2019 (pre COVID-19 pandemic) and Q 4 2021, rental prices have increased by 15.6% for Limerick City and 21.1% for Limerick County (including sub-urban and outer parts of Limerick Metropolitan Area).[3]

Limerick Housing Stock

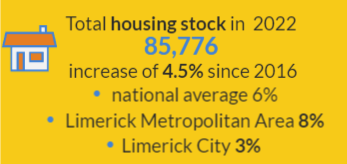

Based on preliminary data from Census 2022, Limerick City and County has a total housing stock of 85,776 units, an increase of 4.5% compared with 2016. This level of growth in the housing stock is below the national average (6%). The rate of growth in the housing stock was faster in the Metropolitan Area (8%) compared with the City and County as a whole and compared with the former city council area (3%).

Areas that show the largest increases in housing stock between 2016 and 2022 are in the Metropolitan Area and mostly in or close to the suburbs – in the Electoral Divisions of Limerick South Rural (+26%), Ballysimon (+14%) and Clarina (+16%).

Electoral Divisions in the city where the housing stock increased at faster rates are Prospect A (Lord Edward Street, Bourke Avenue connected to a new social housing scheme) (+15%) and Shannon B (inner city around Catherine Street, Glentworth Street) (+13%).

The number of vacant dwellings in Limerick City and County in 2022 was 6,643 – as reported above. This is a vacancy rate of 7.7% (national average 7.8%). Bringing vacant dwellings back into use as housing is an important agenda at national and local level.

Housing Tenure

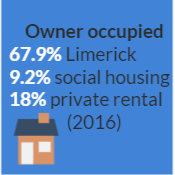

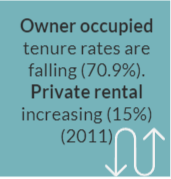

Home ownership rates in Ireland are high by European standards. In Limerick City and County, 67.9% of housing is owner-occupied either owned outright or with a mortgage, 9.2% is social housing (local authority housing and housing cooperatives) and 18% private rental housing (2016). The trend has been towards falling owner-occupied tenure (from 70.9% in 2011 to 67.9% in 2016) and increasing private rental tenure (15% in 2011 to 18% in 2016) for Limerick City and County.

The proportion in different types of tenure varies by sub-area.

The proportion in different types of tenure varies by sub-area.

There are higher rates of home ownership in the former Limerick County (67.9% in 2016) with the highest rates in the rural Metropolitan Districts (81.3% in Adare-Rathkeale, 79.7% in Cappamore-Kilmallock and 73.4% in Newcastle West MD) compared with Limerick Metropolitan Area (59.4%). Home ownership rates in older working class communities in the city are relatively high, reflecting the policy of local authority housing tenants becoming home owners under Tenant Purchase Schemes.

Private rental and social housing tenure rates are higher in the city and wider Metropolitan Area. Social housing tenure rates are highest in the former Limerick City Council area (12%) and Limerick Metropolitan (10.9%) compared with rural Metropolitan Districts: Adare-Rathkeale MD (6.2%), Newcastle West MD (8.4%) and Cappamore-Kilmallock MD (7%).

Private rental and social housing tenure rates are higher in the city and wider Metropolitan Area. Social housing tenure rates are highest in the former Limerick City Council area (12%) and Limerick Metropolitan (10.9%) compared with rural Metropolitan Districts: Adare-Rathkeale MD (6.2%), Newcastle West MD (8.4%) and Cappamore-Kilmallock MD (7%).

Social housing rates in the most disadvantaged areas of the city are higher than average rates for Limerick urban area - highest in the more recently constructed social housing estates (Moyross, 64%) compared with older estates (41% for St. Mary’s Park and 25% for Ballinacurra Weston).

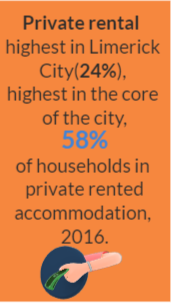

In the former Limerick City, private rental accommodation accounts for just under one-quarter of all tenure types in 2016. Rates of private rental accommodation are highest in the city centre. For instance, in the core of the city (with a population of just under 10,000), 58% of households are private rental accommodation. It should be noted that some of those households in private rented accommodation are supported by the state under rent subsidy / support schemes (the Rental Accommodation Scheme (RAS) and the Housing Assistance Payment (HAP)). These state schemes subside rents when social housing is not available in the current stock (as is the situation at present).

In the former Limerick City, private rental accommodation accounts for just under one-quarter of all tenure types in 2016. Rates of private rental accommodation are highest in the city centre. For instance, in the core of the city (with a population of just under 10,000), 58% of households are private rental accommodation. It should be noted that some of those households in private rented accommodation are supported by the state under rent subsidy / support schemes (the Rental Accommodation Scheme (RAS) and the Housing Assistance Payment (HAP)). These state schemes subside rents when social housing is not available in the current stock (as is the situation at present).

This means that some of the private rental market is in fact quasi social housing.

In local residential areas, tenure / income and social mix is considered important in building sustainable communities. This principle informs current developments in and allocations to social housing.

Future Housing Need Limerick

Based on a study to assess future housing needs and demand in Limerick conducted in 2020, to input to the preparation of the Limerick Development Plan 2022-2028, housing demand over the six-year plan period to 2028 is determined to be 15,591 housing units, or 2,598 units per annum.[4] Housing supply will need to be developed to meet different requirements in terms of the physical locations of new housing, and be consistent with overall spatial planning policies. These requirements include: achieving compact growth or housing development within the footprint of the city to achieve population growth for the inne r city area (the “living city”) and within towns and village settlements. Investment in waste water and water infrastructure / services capacity and other infrastructure are essential to allow for housing development as there is a lack of capacity in such infrastructure in many settlements in Limerick.

r city area (the “living city”) and within towns and village settlements. Investment in waste water and water infrastructure / services capacity and other infrastructure are essential to allow for housing development as there is a lack of capacity in such infrastructure in many settlements in Limerick.

Increase in housing supply will need to take into account climate change considerations in terms of access transport / transport services, locations of work and recreation and energy efficiency of building and environment. Social aspects include consideration of needs of people with different levels of income, at different stages of the life course including young people, new families and older people downsizing, people with disabilities (physical, sensory and with specific health conditions) and Traveller accommodation. Size and types of unit and tenure mix (private, social, affordable) are further relevant considerations in the creation of sustainable communities. There are significant challenges associated with delivery of this level of supply and complexities associated with different types of need.[5]

Limerick’s Social Housing Stock & Targets for Social & Affordable Housing

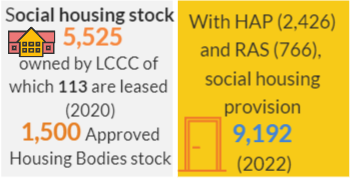

Data for Q4 2020 indicates that Limerick City and County Council owns 5,525 housing units, of which 113 are leased. Approved Housing Bodies (AHBs) - voluntary and communities bodies that respond to housing need – operate in Limerick (52 AHBs in 2022). The total AHB stock in Limerick is approximately 1,500 units. Social housing need is also addressed through the private rental market  under the Rental Accommodation Scheme (RAS) (766 Private RAS properties at end of year 2021) and the Housing Assistance Payment (2,426 at end of year 2021). Across the different social housing options, the number of households in these forms of social housing provision in Limerick in 2022 is 9,191.[6]

under the Rental Accommodation Scheme (RAS) (766 Private RAS properties at end of year 2021) and the Housing Assistance Payment (2,426 at end of year 2021). Across the different social housing options, the number of households in these forms of social housing provision in Limerick in 2022 is 9,191.[6]

Each local authority in the state is set targets for the period 2022-2026 for delivery of social and affordable housing units under government’s strategy, Housing for All. The social housing target for Limerick City and County by 2026 is 2,693 homes, of which approximately 60% are to be delivered directly by the local authority (1,615) and 40% by AHBs (1,077). The Council’s approach to this is to deliver new build social housing (rather than buying existing housing for long-term lease). Currently, 1,220 housing units have been approved and 1,616 are at pre-approval stage. In 2022, 474 new social housing units are underway. Between the years 2022-2026, the Council’s target for affordable housing is 1,264 units, approximately 253 per year. Of this target, 264 units are for direct delivery by the local authority. Other delivery agencies are the Land Development Agency and Approved Housing Bodies.

Social Housing Need & the Housing “Waiting List”

Limerick City and County Council carries out assessments of social housing need and follows a process to qualify applicants for social housing. The number approved or qualified for social housing in Limerick in 2022 is 2,238. This is the “net” housing need as it excludes those households awaiting transfers and those in private rented a ccommodation supported under the HAP/RAS. The “gross” number on the “housing waiting list” is 5,863 including those awaiting transfers and on HAP/RAS.

ccommodation supported under the HAP/RAS. The “gross” number on the “housing waiting list” is 5,863 including those awaiting transfers and on HAP/RAS.

Current demand for social housing based on the housing waiting list for Limerick City and County shows highest demand in the city and within the city, stronger in the electoral area of Limerick City East. One and two-bed units are the most sought after in all areas. There is little demand for 4+ bed unit types.

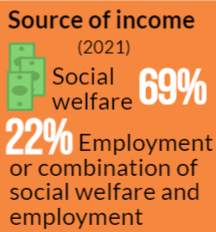

In terms of characteristics of those qualified for housing support in Limerick, based on 2021 data, 69% are dependent on social welfare as their only source of income while 22% have income from employment only or a combination of employment and social welfare income. The percentage reliant on social welfare income only is significantly smaller compared with 10 years ago where this was at 80%. This situation reflects changes in the labour market (more jobs) and in social welfare schemes as well as the significant difficulties in the current housing market.

In terms of characteristics of those qualified for housing support in Limerick, based on 2021 data, 69% are dependent on social welfare as their only source of income while 22% have income from employment only or a combination of employment and social welfare income. The percentage reliant on social welfare income only is significantly smaller compared with 10 years ago where this was at 80%. This situation reflects changes in the labour market (more jobs) and in social welfare schemes as well as the significant difficulties in the current housing market.

In terms of basis for the need, only 16% state reliance on rent supplement while half (50%) state unsuitable household circumstances (37%) or requirement for separate accommodation (13%). This is consistent with analysis of current living arrangements of qualifying applicants where 41% are either living with their parents or relatives and friends in over-crowded or unsuitable conditions. Over half (53%) have a household size of only one adult and 4% an adult couple. This is consistent with strongest demand for one-bed or two-bed units. Just under one-quarter of qualifying applicants are under 30 years, while 30% are aged 30-39 years.

In terms of basis for the need, only 16% state reliance on rent supplement while half (50%) state unsuitable household circumstances (37%) or requirement for separate accommodation (13%). This is consistent with analysis of current living arrangements of qualifying applicants where 41% are either living with their parents or relatives and friends in over-crowded or unsuitable conditions. Over half (53%) have a household size of only one adult and 4% an adult couple. This is consistent with strongest demand for one-bed or two-bed units. Just under one-quarter of qualifying applicants are under 30 years, while 30% are aged 30-39 years.

More than two-thirds (68%) of qualifying applicants have no specific accommodation requirements. However, 15% are homeless, 11% have an enduring physical health, mental health or intellectual issue, 5% require Traveller accommodation and 1% is old age-related (65 years and over).

In terms of the length of time on the housing waiting list, one-quarter of qualifying applicants are over seven years on the waiting list while over one-third (36%) are over five years on the waiting list.

Homelessness

In the last week of September 2022, in Limerick there were 330 homeless adults accommodated in emergency accommodation funded andoverseen by housing authorities. The trend in homelessness in the state and in Limerick is upwards. Across Limerick and Clare County, there were 91 families homeless in emergency accommodation in the same period (September 2022). Three-quarters of these were single parent families. Within these families, there were 124 adults and 180 dependent children.[7]

[1] Data from Limerick City and County Council (2021). Limerick City and County Housing Strategy and HNDA 2022-2028. Incorporated into the Limerick Development Plan 2022-28. https://www.limerick.ie/sites/default/files/media/documents/2021-06/volume-6-limerick-city-and-county-draft-housing-strategy-and-housing-need-demand-assessment.pdf

[2] Data from Mid-West Economic Insights, Spring 2022. Limerick Chamber

[3] Based on data from www.daft.ie reported in Mid-West Economic Insights, Spring 2022. Limerick Chamber.

[4] See Volume 6 Limerick Development Plan 2022-2028, Limerick City and County Housing Strategy and Housing Need Demand Assessment 2022-2028 https://www.limerick.ie/sites/default/files/media/documents/2022-07/Housing-Strategy-and-Housing-Need-Demand-Assessment.pdf

[5] See Limerick City and County Council’s Housing Delivery Action Plan 2022-2026, setting out details of planned social and affordable housing delivery under Government’s Housing for All. https://www.limerick.ie/council/services/housing/housing-delivery/housing-delivery-action-plan

[6] Data from the Housing Agency Data Hub. https://www.housingagency.ie/data-hub/welcome-housing-agency-data-hub